Mortgage rates have been one of the biggest reasons many buyers and homeowners have stayed on the sidelines. After years of higher borrowing costs, even a small move lower can make people wonder the same thing:

Is now the time to make a move?

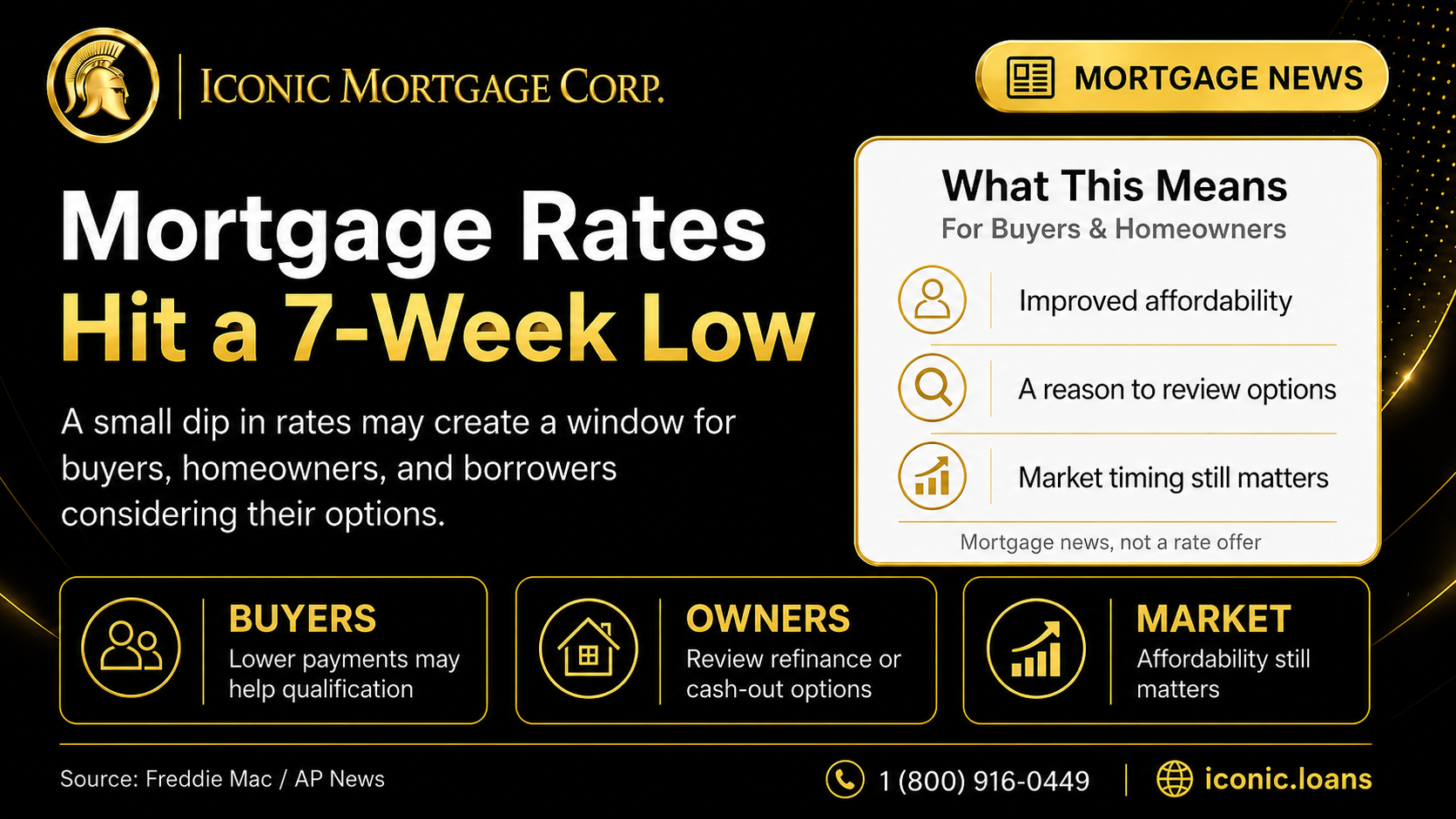

According to AP News, the average 30-year fixed mortgage rate recently fell to 6.43%, down from 6.49% the week before. That marks the lowest level since mid-May. The average 15-year fixed mortgage rate also moved lower, falling to 5.79%.

That does not mean mortgage rates are suddenly low. It does mean borrowers may have a better opportunity than they had just a few weeks ago.

Why This Rate Drop Matters

Mortgage rates affect more than just the interest charged on a loan. They directly impact monthly payment, buying power, refinance opportunities, and the amount of home a borrower may qualify for.

For homebuyers, a lower rate can help reduce the monthly payment or improve qualification. For homeowners, it may be a reason to review whether refinancing, consolidating debt, or accessing home equity makes sense.

Even a modest rate drop can make a difference, especially for borrowers who were close to qualifying or homeowners who have been waiting for a better time to review their options.

Rates Are Lower, But Affordability Is Still a Challenge

The recent dip is good news, but affordability is still a major issue in the housing market. Home prices remain elevated in many areas, and mortgage rates are still much higher than the historically low rates borrowers saw during the pandemic years.

Existing home sales remain well below their historical norm, even though there has been some improvement in activity. Buyers and sellers are also beginning to accept mid-6% mortgage rates as closer to the current normal, but affordability continues to hold many people back.

That is why the right question is not simply, “Are rates low?”

The better question is:

“Does the payment, loan structure, and long-term plan make sense for me right now?”

Should Buyers Wait for Rates to Fall More?

Waiting for a lower rate sounds logical, but it can be risky. Mortgage rates can move quickly based on inflation, bond yields, Federal Reserve expectations, and overall economic conditions.

Rates are not guaranteed to keep falling.

For buyers, waiting could help if rates move lower. But waiting could also mean higher home prices, more competition, fewer available homes, or a rate increase that wipes out the benefit of waiting.

The best move is usually not trying to perfectly time the market. It is understanding your numbers clearly so you can act when the right opportunity is available.

What This Means for Homeowners

Homeowners should also pay attention to rate changes. A lower average rate may open the door for some borrowers to review refinance options, especially if they currently have a higher-rate mortgage, need to consolidate higher-interest debt, or want to access equity for a specific financial goal.

That does not mean refinancing is right for everyone. The numbers depend on your current interest rate, loan balance, credit profile, equity position, loan type, closing costs, and how long you plan to keep the loan.

For some homeowners, the better option may not be a full refinance. A home equity loan, HELOC, or cash-out refinance may be worth comparing depending on the goal.

A Small Window Can Still Be Worth Reviewing

This latest rate drop does not change the entire market overnight. But it may create a window for borrowers who were already thinking about buying, refinancing, or using home equity.

The key is to compare the real numbers.

A mortgage review can help answer questions like:

- Is my current rate still competitive?

- Would a refinance save money or improve cash flow?

- Can I qualify for more home than I could a few weeks ago?

- Would consolidating debt through home equity make sense?

- Should I lock now or keep watching the market?

Bottom Line

Mortgage rates have moved lower, with the average 30-year fixed rate reaching its lowest level in seven weeks. That is encouraging news for buyers and homeowners, but it does not mean everyone should rush into a loan.

The best decision depends on your personal numbers, goals, and timeline.

If you have been waiting for a better time to review your mortgage options, this may be a smart moment to take a fresh look.

Iconic Mortgage Corp. can help you compare your options and see what makes sense based on your situation.

Disclaimer: Mortgage rates change frequently and depend on borrower qualifications, loan type, credit profile, property type, loan-to-value, and other factors. This article is for informational purposes only and is not a commitment to lend.